03 June 2022

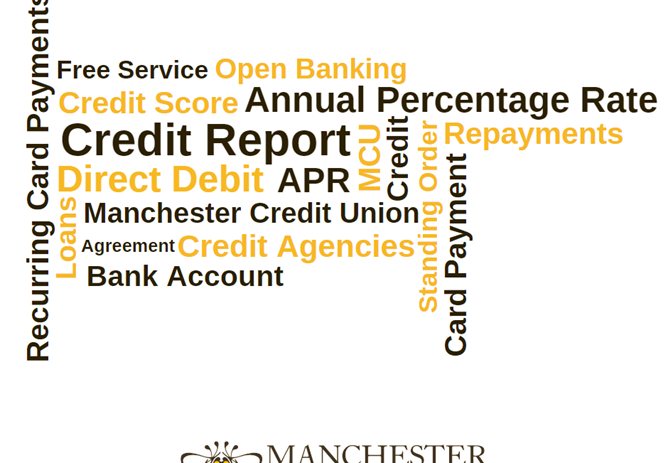

Demystifying financial terminology

There is no doubt that understanding your finances can be complicated and this isn’t helped by the amount of jargon used by financial institutions. At the moment, schools in the UK do not teach students about financial matters which means when they leave school, they have little idea how to manage their finances when they find a job and look for a home.

As a member of MCU, you will become aware of phrases and terminology in your dealings with us so here are a few you may come across with explanations to help you understand.

Credit Report - A credit report is a record of your credit history. It includes your current and previous addresses, history of repayments, county court judgements or bankruptcies, and other financial commitments you have. You can check your credit score by getting your credit report from one of the UK’s credit agencies. Most offer a free service, check out these popular options;

- Credit karma https://www.creditkarma.co.uk/

- clearscore https://www.clearscore.com/

Credit Score – also known as Credit Rating. This is part of your Credit Report. If you need credit, a good credit score may help your application. To improve your score, ensure you are on the electoral role, pay your bills on time, use a credit card wisely and don’t make too many applications for credit as this will affect your score.

Annual Percentage Rate (APR) – This is important because it lets you compare one loan offer against another. When you take out a loan, you should always see an APR quoted to you. The APR tells you the total cost you will pay for your borrowing. The lower the APR, the cheaper the loan repayments. At MCU the APR we offer is guaranteed not representative meaning you will know exactly how much the loan will be.

Standing Order – You have control of this arrangement; you are asking your Bank to make automatic and regular payments of the same amount. For example, if you wanted to save £10 per month in your MCU savings account, you would set the standing order up so your Bank would transfer the money each month from your Bank account to your MCU account.

Direct Debit – This is an arrangement between you and whoever you are paying. It’s a bit like a Standing Order, but in this case, you ask your bank to allow an organisation to take the payments from your account. The amount and frequency can vary, depending on who you are paying.

Recurring Card Payments – This works like a direct debit, but instead of taking payments from your bank account, under a recurring card payment agreement, regular payments are taken from your debit card for agreed amounts on agreed dates. If you enter into this kind of arrangement, it’s important you let who you’re paying know if you get a new debit card as the account details on the new card will change.

Open Banking – when you apply for a loan with MCU we will ask you to register and consent to Open Banking which allows us to securely view your financial data to help us decide whether we can provide you with credit. We can only view the data, we can’t change it or take payments from your account.